U.S. single-family homebuilding tumbled in March as a resurgence in mortgage charges pushed potential patrons to the sidelines. In keeping with the U.S. Census Bureau, housing begins dropped by 14.7% in March to 1.321M vs. 1.480M anticipated and 1.549M prior (revised from 1.521M). Single-family housing begins ran at a fee of 1.022M, 12.4% under the revised February determine of 1.167M. Constructing permits additionally slid greater than anticipated, falling by 4.3% M/M to 1.458M vs. 1.510M anticipated and 1.523M prior (revised from 1.518M).

In keeping with the Nationwide Affiliation of Residence Builders (NAHB)/Wells Fargo Housing Market Index (HMI) launched just lately, “sentiment was flat in April as mortgage charges remained near 7% over the previous month and the most recent inflation information failed to indicate enchancment throughout the first quarter of 2024.

Get the clearest, most correct view of the truckload market with information from DAT iQ.

Tune into DAT iQ Reside, dwell on YouTube or LinkedIn, 10am ET each Tuesday.

“With many pissed off patrons again on the fence ready for rates of interest to fall, policymakers may help ease affordability challenges by decreasing inefficient regulatory guidelines that increase housing prices and restrict provide,” stated NAHB Chairman Carl Harris, a customized dwelling builder from Wichita, Kan.

“April’s flat studying suggests the potential for demand progress is there, however patrons are hesitating till they will higher gauge the place rates of interest are headed,” stated NAHB Chief Economist Robert Dietz. “With the markets now adjusting to charges being considerably increased resulting from latest inflation readings, we nonetheless anticipate the Federal Reserve will announce future fee cuts later this 12 months and that mortgage charges will average within the second half of 2024.”

Market watch

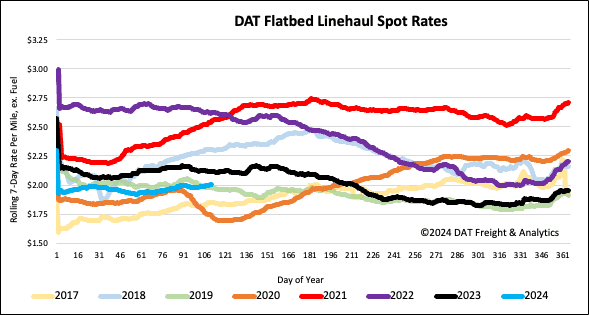

All charges cited under exclude gasoline surcharges until in any other case famous.

Though the overall variety of oil and gasoline drilling rigs has been flat because the begin of the 12 months, in keeping with Baker Hughes, rig counts are up 2% within the West Texas Permian Basin, the place 51% of rigs are positioned. Supplying this area with drill pipe and casing is primarily the Houston freight market, the place masses moved are up 14% y/y following final week’s 12% w/w enhance.

Outbound linehaul charges in Houston have elevated by $0.07/mile within the final month. On the primary lane west to Lubbock within the Permian Basin, flatbed carriers had been paid a median of $2.13/mile final week. On the quantity two lane to El Paso, linehaul charges had been flat, averaging $2.39/mile on a 13% increased quantity of masses moved.

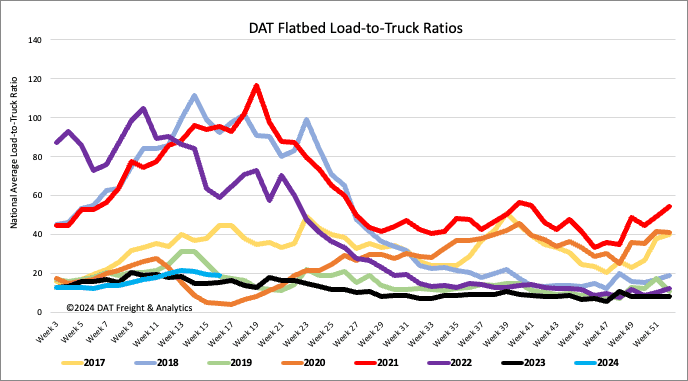

Load-to-Truck Ratio

Flatbed load put up volumes fell for the fourth week following final week’s 4% w/w lower. Volumes are 4% decrease than final 12 months and similar to 2019. Like dry van and reefer, flatbed gear posts elevated beneath 5% w/w, lowering the load-to-truck ratio by 4% to 18.94.

Spot charges

Flatbed linehaul charges remained primarily flat to down barely for the second week, averaging just below $2.02/mile. In comparison with final 12 months, the nationwide common is $0.12/mile decrease and $0.02/mile increased than 2019.

{kind=link}