In April, residential housing building for single-family properties was largely flat sequentially however nonetheless 22% greater than final 12 months. For flatbed carriers on the lookout for demand alerts of an enhancing truckload market, the April outcome exhibits the market is in a holding sample now the Federal Reserve has indicated price cuts might not happen this 12 months as anticipated.

Get the clearest, most correct view of the truckload market with information from DAT iQ.

Tune into DAT iQ Stay, dwell on YouTube or LinkedIn, 10am ET each Tuesday.

In keeping with the U.S. Census Bureau, begins had been at an annual price of 1.36 million, 5.7% greater than the downwardly revised March variety of 1.29 million. Permits, in the meantime, got here in at 1.44 million, down from the upwardly revised 1.485 million in March. Each had been barely beneath the comparable month in 2023.

“Nevertheless, homebuilders are beginning to really feel much less assured as mortgage charges hover round 7% and client confidence begins to weaken. This 12 months permits for developing new single-family properties reflecting future constructing exercise are additionally greater. Nonetheless, the year-over-year improve in allow exercise has slowed,” stated Brilliant MLS Chief Economist Lisa Sturtevant.

For flatbed carriers, April’s building of 1.3 million single-family properties translated into roughly 620,000 masses, 110,400 greater than April final 12 months and 74,000 extra masses than the booming 2018 flatbed market.

Market watch

All charges cited beneath exclude gas surcharges until in any other case famous.

U.S. power companies added oil and pure gasoline rigs for the primary time in 4 weeks this week, in response to Power Companies agency Baker Hughes’s carefully adopted report on Friday. The oil and gasoline rig rely, an early indicator of future flatbed demand, rose by one to 604 within the week to Might 17. Regardless of this week’s rig improve, Baker Hughes stated the entire rely was nonetheless down 116, or 16% beneath this time final 12 months. Round half of the rig rely is positioned within the West Texas Permian Basin, within the Lubbock freight market serviced primarily by flatbed capability in Houston.

The amount of masses shifting on the Houston to Lubbock lane was down 9% final week, whereas spot charges jumped by $0.15/mile to a median of $2.57/mile, simply over $0.25/mile decrease than final 12 months. The identical quantity of masses moved. Houston to El Paso charges had been up $0.10/mile w/w to $2.51/mile on a 13% decrease quantity. The Houston market recorded a $0.07/mile improve in spot charges final week, averaging $2.20/mile for outbound masses.

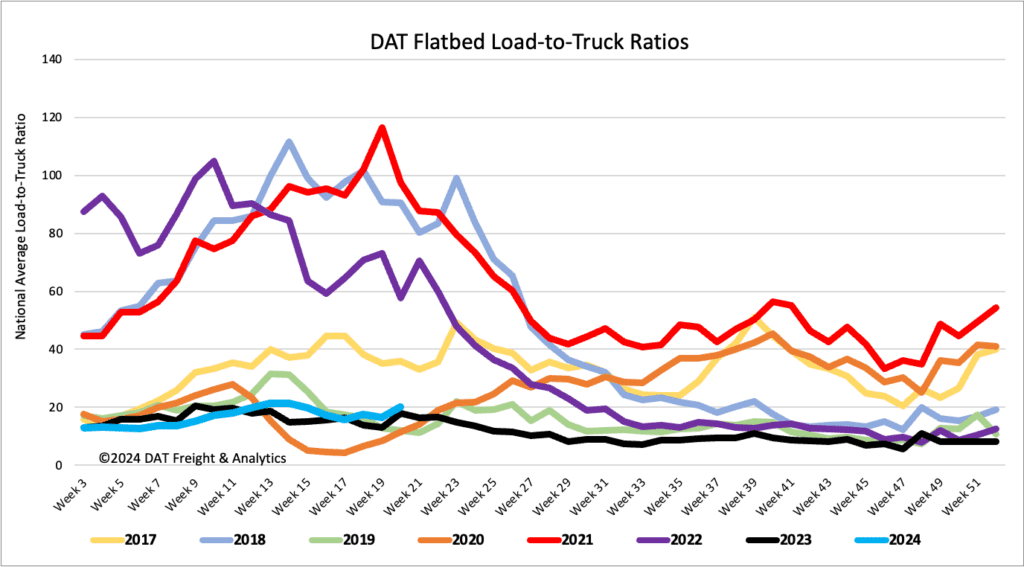

Load-to-Truck Ratio

Flatbed load publish volumes elevated by 8% w/w, whereas tools posts dropped by 11% w/w, rising the load-to-truck ratio by 22% to twenty.05

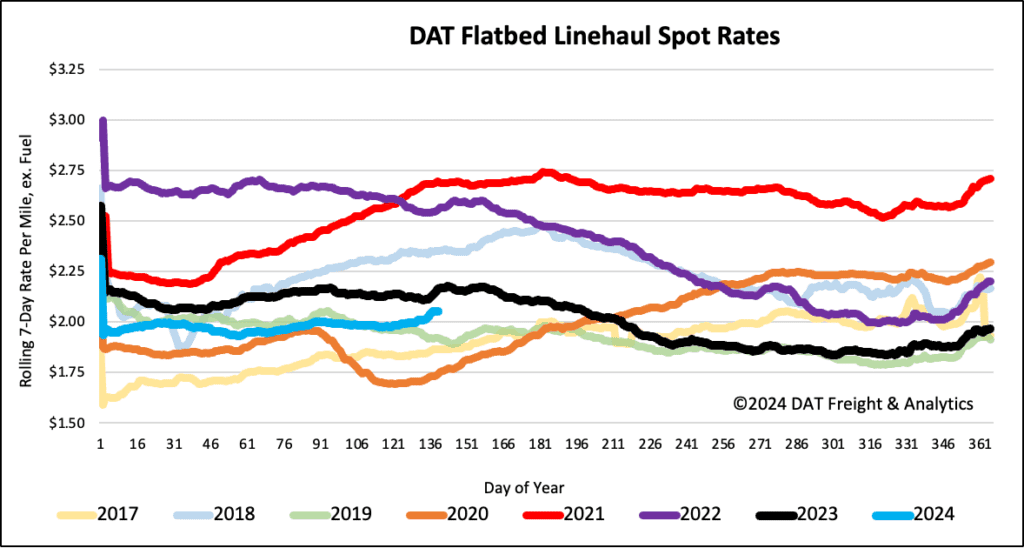

Spot charges

After remaining flat for 3 weeks, flatbed linehaul charges elevated by $0.03/mile final week to a nationwide common of $2.06/mile. The nationwide common is $0.11/mile decrease resulting from an 18% greater quantity of masses moved than final 12 months.

{kind=link}